© phasinphoto Fotolia.com

In 2013, Chris had inexpensive health insurance. His premiums were only $200 each month. That sounds pretty good, especially since average premiums for a single person are more than $400 per month.

This is the one of a series of articles on understanding health insurance. Click here for all of the articles. This series covers basics — exceptions and complications go beyond the basics.

Trouble was — Chris’s actual health care costs were a lot higher. Besides paying the premium, he had to pay $3,000 of medical costs out of his pocket before the insurance paid a dime. Premiums are just one of the costs to look at when you buy health insurance.

That’s true whether you are buying employer-sponsored health insurance or private health insurance. It’s true whether you are buying from a broker or through MNSure.

Definitions

Premium: the amount you pay each month for health insurance coverage.

Deductible: the amount you pay for health care each year BEFORE your insurance company pays anything.

To figure out what insurance plan is best for you and your family, you need to look at more than premiums. Consumer Reports advises looking at:

- What does the plan cover?

- How much does the plan cost?

- Which doctors and hospitals are in it?

Good questions! In this post and the next, we’ll look at what plans really cost.

Premiums

Each person or family pays premiums monthly. Premiums are lower for individual coverage and higher for family coverage.

If you have an employer-sponsored plan, your employer might pay part or all of your premium. Often, you can choose between different plans, which have different coverage and different premiums. Two-thirds of Minnesotans get health care through employer-sponsored plans.

If you do not have an employer-sponsored plan, you can buy private insurance from a broker or insurance company or through MNSure. If your income is low, you can also enroll in public insurance through MNSure — this might be Medicaid or MinnesotaCare.

What color is your MNSure plan?

MNSure classifies insurance plans by color. The lowest cost plan is bronze, then silver, gold and platinum. The lowest cost plan — bronze — also gives you less. Bronze plans pay an average of 60 percent of health care costs. That means that if your doctor bill is $300, the plan will pay $180 and you will pay $120. (There are other complications, but we’ll get to those in the post covering deductibles, co-payments and co-insurance.)

Silver plans pay, on average, 70 percent of health care expenses; gold plans pay 80 percent; and platinum plans pay 90 percent.

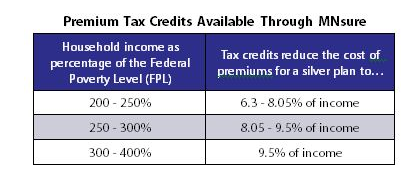

Table from MNSure website – http://www.mnbudgetproject.org/research-analysis/economic-security/health-care/mnsure-a-new-world-of-opportunities-for-affordable-health-insurance-starting-in-2014

If you earn less than four times the federal poverty level, you can get federal tax credits to help pay for part of the premium expense for a silver plan.

Definitions

Federal poverty level: The federal government defines the poverty level, which changes according to the number of people in your family. Click here for 2014 poverty levels. (Or scroll down to the bottom of the page.)

Beyond the premium

The premium is what you pay for health insurance. Health insurance will pay a big part of your health care costs. The part that you have to pay can be pretty big, too. Here’s the equation:

Premium + deductibles + co-payments + co-insurance = your health care cost

We’ll look at that next in Putting together the puzzle: Deductibles, copayments, co-insurance, out-of-pocket limit.

Complications

When it comes to insurance, nothing is simple. This series covers basics — exceptions and complications go beyond the basics. Catastrophic coverage is an example of a complicated premium question. People under 30 and some over 30 with a “hardship exemption” can buy a catastrophic plan. That means lower premiums, but you pay all health care costs up to a very high deductible amount.

More information:

- Trouble ahead? Three health insurance alerts

- Open enrollment time: Should you renew or change your health insurance?

- Beyond the premium: What will you really pay for health care?

- Putting together the puzzle: Deductibles, copayments, co-insurance, out-of-pocket limit

- What you need to know about health insurance bills, networks and tiers

- What does health insurance cover?

- If you can’t afford health insurance … three ways to get help

- Key questions: Choosing your family’s health insurance

Federal poverty levels in 2014:

• $11,670 for individuals

• $15,730 for a family of 2

• $19,790 for a family of 3

• $23,850 for a family of 4

• $27,910 for a family of 5

• $31,970 for a family of 6

• $36,030 for a family of 7

• $40,090 for a family of 8

Discover more from News Day

Subscribe to get the latest posts sent to your email.

Pingback: Putting together the puzzle: Deductibles, copayments, co-insurance, out-of-pocket limit | News Day

Pingback: What you need to know about health insurance bills, networks and tiers | News Day

Pingback: What does health insurance cover? | News Day

Pingback: If you can’t afford health insurance … three ways to get help | News Day

Pingback: Open enrollment time: Should you renew or change your health insurance? | News Day

Pingback: Key questions: Choosing your family’s health insurance | News Day