© John Takai – Fotolia.com

I couldn’t believe the bill — $447 for a single office visit. Even worse, the bill said my share was $168. I thought my deductible was $75, so that seemed like too much. As I always do when faced with puzzling bills, I called the insurance company.

This is the one of a series of articles on understanding health insurance. Click here for all of the articles. This series covers basics — exceptions and complications go beyond the basics.

Decoding the bill

The woman on the help line patiently went through the bill.

First, there were the two amounts that the clinic charged. One was for an annual check-up. That’s fully covered as preventive care, so the insurance company pays it all.

The second amount was for some other advice. Months later, I’m not even sure what it was, but evidently there was a consultation on something beyond the scope of the preventive annual checkup. That is not fully covered, so I will have to pay the deductible amount.

Definitions

Deductible: the amount you pay for health care each year BEFORE your insurance company pays anything. See Putting together the puzzle: Deductibles, copayments, co-insurance, out-of-pocket limit for more explanation.

But, I said, my deductible is only $75. I checked in the big booklet explaining my policy. What’s up?

Networks and choices

What’s up turns out to be networks and payment levels.

Our insurance company decides whether health care providers are in-network or out-of-network. If they are in-network, we’re covered. If they are out-of-network, we’re not. (Except — the usual disclaimer — it’s complicated. See “Making choices” below.)

Do you care what doctor you see? Or what clinic you go to? If you do, it’s important to check the network when you choose an insurance plan.

Some plans have very narrow networks. That means fewer choices for you. Some plans may have a wider network — but not the doctor your children have been seeing since they were born.

Our clinic, doctors, specialists, etc. are all in-network, so we’re covered. Then the story gets complicated. The health insurance representative on the phone explained about tiers or cost levels. Even in-network providers are not all treated the same. The insurance company decides on different levels of payment for different providers.

Our primary care clinic is in the second level. That means a higher deductible than the first level. For the second level, the deductible is $180 per individual/$360 for the family. Therefore I owed $126.68, since that is less than the deductible.

If we had chosen a primary care clinic in the lowest cost level, we would have a lower deductible. That’s not a good option for us. Staying with the doctors we know and trust is more important.

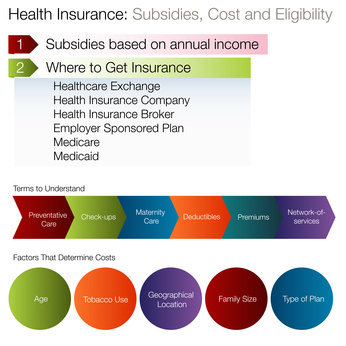

Making choices: What plan is right for you?

You might think that choosing a doctor begins when you need a doctor. That’s not quite true. When you choose an insurance plan, your choices are restricted by the plan. Insurance comes in different kinds of plans.

A Health Maintenance Organization (HMO) requires you to use only the doctors in the organization. Within the HMO, you will choose a Primary Care Physician, and will only go to other HMO providers with a referral from that physician. This is the most restrictive kind of plan.

A Preferred Provider Organization (PPO) allows you to choose in-network health care providers. You may also be able to get care from out-of-network providers, but you will pay more of the cost.

Other kinds of plans include Exclusive Provider Organization (EPO), Point of Service (POS), and more. For information, see this Healthcare.gov page or this insurance guide for small businesses.

Tiers of coverage and formularies

Insurance companies pay for some medicines, and not for others. They pay different amounts for different medicines. Prescription medicines may cost you a $10 deductible each time you refill the prescription, or they may cost thousands of dollars every month. If someone in your family must take medications regularly, it’s important to check on what the insurance company will pay for.

A formulary is the name for a list of medications that the insurance company will pay for. The formulary is organized in “tiers” or levels. Tier One includes the drugs with the lowest co-payment. These are usually generic (non-brand-name) drugs. Tier Two includes some generic and some brand-name drugs, and the co-payment is higher. Costs keep on going up through the tiers.

Formularies change. If you know what medications your family needs, it’s important to review the formulary each year to check for changes.

Complications

When it comes to insurance, nothing is simple. This series covers basics — exceptions and complications go beyond the basics.

Deductibles and co-pays: Different deductibles and co-pays apply for different services — lab services, emergency room visits, specialists, physical therapy all may have different co-pays or co-insurance. That’s another reason to check and compare policies. If you know that a family member needs regular doctor visits or physical therapy, one policy may offer better coverage. See Putting together the puzzle: Deductibles, copayments, co-insurance, out-of-pocket limit for more explanation.

What the insurance company pays: The insurance company usually doesn’t pay full price. They have pre-set amounts they agree to pay for different services. Health care providers have agreed to accept this lower amount.

Our clinic bill lists two amounts. The first is the amount the clinic charged, and the second is the amount the insurance company “allowed.” That’s the amount the insurance company pays.

- Trouble ahead? Three health insurance alerts

- Open enrollment time: Should you renew or change your health insurance?

- Beyond the premium: What will you really pay for health care?

- Putting together the puzzle: Deductibles, copayments, co-insurance, out-of-pocket limit

- What you need to know about health insurance bills, networks and tiers

- What does health insurance cover?

- If you can’t afford health insurance … three ways to get help

- Key questions: Choosing your family’s health insurance

Discover more from News Day

Subscribe to get the latest posts sent to your email.

Pingback: Beyond the premium: What will you really pay for health care? | News Day

Pingback: What does health insurance cover? | News Day

Pingback: Putting together the puzzle: Deductibles, copayments, co-insurance, out-of-pocket limit | News Day

Pingback: If you can’t afford health insurance … three ways to get help | News Day

Pingback: Open enrollment time: Should you renew or change your health insurance? | News Day

Pingback: Key questions: Choosing your family’s health insurance | News Day